As a constant fixture within the commodity markets, gold carries an unusual relationship: a positive correlation with inflation. Of course, any non-cash asset technically has a positive relationship with inflation because inflation means rising prices (hence, when inflation goes up non-cash assets go up and vice versa). In the case of gold, however, this relationship goes beyond a one-to-one correlation and becomes a leveraged correlation with inflation. That is, this metal is typically expected to rise more than the rate of inflation due to its role as a store of value.

Notably, although other metals like silver posses this anti-inflationary feature, gold most directly fills the role of a monetary metal/store of value. This article provides reasoning for the relationship between gold and inflation as well as potential use cases for traders.

Why does gold outperform during periods of inflation?

Having established the relationship between inflation and gold prices, it is critical to evaluate the reasons for that relationship. Generally, gold prices benefit from inflation because of the metals’ role as a reserve currency and because of a physically constrained supply. Gold has been used as currency across countless societies for thousands of years. Transactions which lacked a trusted paper currency or a direct barter agreement could be settled safely with gold. Even in cases where paper currency was adopted, many paper currencies were redeemable in gold. This development occurred because gold has significant industrial value, is easy to store, and cannot be duplicated (counterfeit replicas are generally easy to identify).

Today, gold still has substantial demand from a variety of industries such as aerospace, dentistry, and of course, jewelry. Furthermore, storage risk has been reduced to an all-time low thanks to ultra-secure vault technology. Accordingly, gold remains a safe haven when confidence/value in paper currency dwindles (which is generally represented by an increase in inflation).

To illustrate by example, imagine a country which is experiencing hyperinflation such that holding cash becomes devastating. Everyone who owns that country’s currency is going to rush to some asset which will not erode in value. Bond’s don’t work unless the interest rates are so high that they compensate for the hyperinflation (this rarely happens). Stocks don’t work because businesses are suffering the economic consequences of hyperinflation and are accordingly in disarray. Most commodities (wheat, oil, corn) are too cumbersome to store in significant quantities or are perishable.

Gold, however, can store tremendous amounts of value without taking up significant storage space or perishing. Knowing this, currency holders will rush to purchase gold and subsequently drive up the price beyond the rate of inflation. This very scenario has repeated throughout history and instilled confidence in the metals’ value as an inflation hedge. Notably, given the forward-looking nature of markets, profiting through gold requires recognizing inflation before it actually occurs or before the market thinks it is going to occur. If everyone already knows that inflation is present or is coming, prices will reflect that knowledge and the opportunity will be lost.

Does gold hedge against all economic downturns?

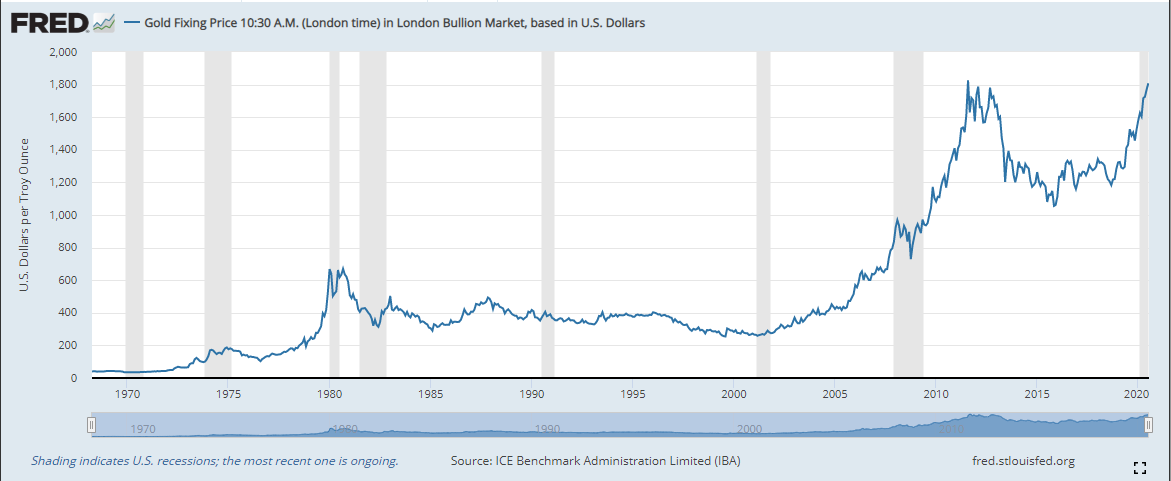

It is worth distinguishing whether gold actually appreciates under generally worsening economic conditions or whether it is strictly an insurance policy against inflation. Given the deflationary nature of many recent recessions (including the recession induced by the ongoing COVID-19 pandemic), understanding precisely what drives the price of this metal is extremely important. The graph below shows the response of gold prices to different U.S. recessions since 1968:

Notice that inside of each recession (shaded areas), the price of gold tends to drop initially before rebounding. In fact, in the most recent recession the price of gold fell by about 12% in two weeks. Of course, it rebounded quite rapidly and is now progressively climbing higher.

This cycle of decline and rebound inside of recessions is typically caused by deflationary expectations as a result of recession followed by inflationary expectations as a result of monetary policy. That is, traders expect deflation at the onset of recessions because of declining velocity of money and later expect inflation because of money-printing by central banks. This trading strategy proved partially effective after the 2008 crisis; many traders bet on inflation while the Federal Reserve continued to announce stimulus programs, however, those programs failed to produce meaningful inflation. The expectation of inflation drove gold prices up but the failure of monetary stimulus to actually deliver inflation eventually led to a price collapse in 2013 (other industrial supply/demand factors also influenced the price heavily).

In conclusion, although many commentators claim that gold is a general hedge against recessions, it frequently depreciates in price at the beginning of recessions. Furthermore, it is illogical for gold to increase in value without an increase in inflation or inflation expectations. After all, gold throws off no income and will actually decline in real value if deflation occurs. Accordingly, traders betting on worsening economic conditions should not assume that gold will automatically profit under such conditions. Instead, inflation expectations should be the driver of gold price predictions (in addition to technical analysis).

The role of gold in a traders toolkit

Traders may want to use gold to bet directly on inflation or to hedge currency exposure. Both of these objectives are well satisfied by gold, however, it is important to remember that, like every commodity, gold is affected by traditional supply and demand factors based on industrial uses and mining capacity. Furthermore, gold should not be used as a vehicle to express deflationary recession expectations.